I am pleased to share with you our latest Market Report for the San Francisco Bay Area. The report begins with economic and real estate commentary presented in partnership with the Rosen Consulting Group (RCG). For the statistical report of the regional housing market, we look at the ten counties associated with the SF Bay Area, focusing primarily on detached single-family homes, with added coverage of the significant condominium market in San Francisco. Enjoy the information and insight provided in the report and I look forward to discussing the market with you.

SF BAY AREA RESIDENTIAL MARKET SPRINGS FORWARD

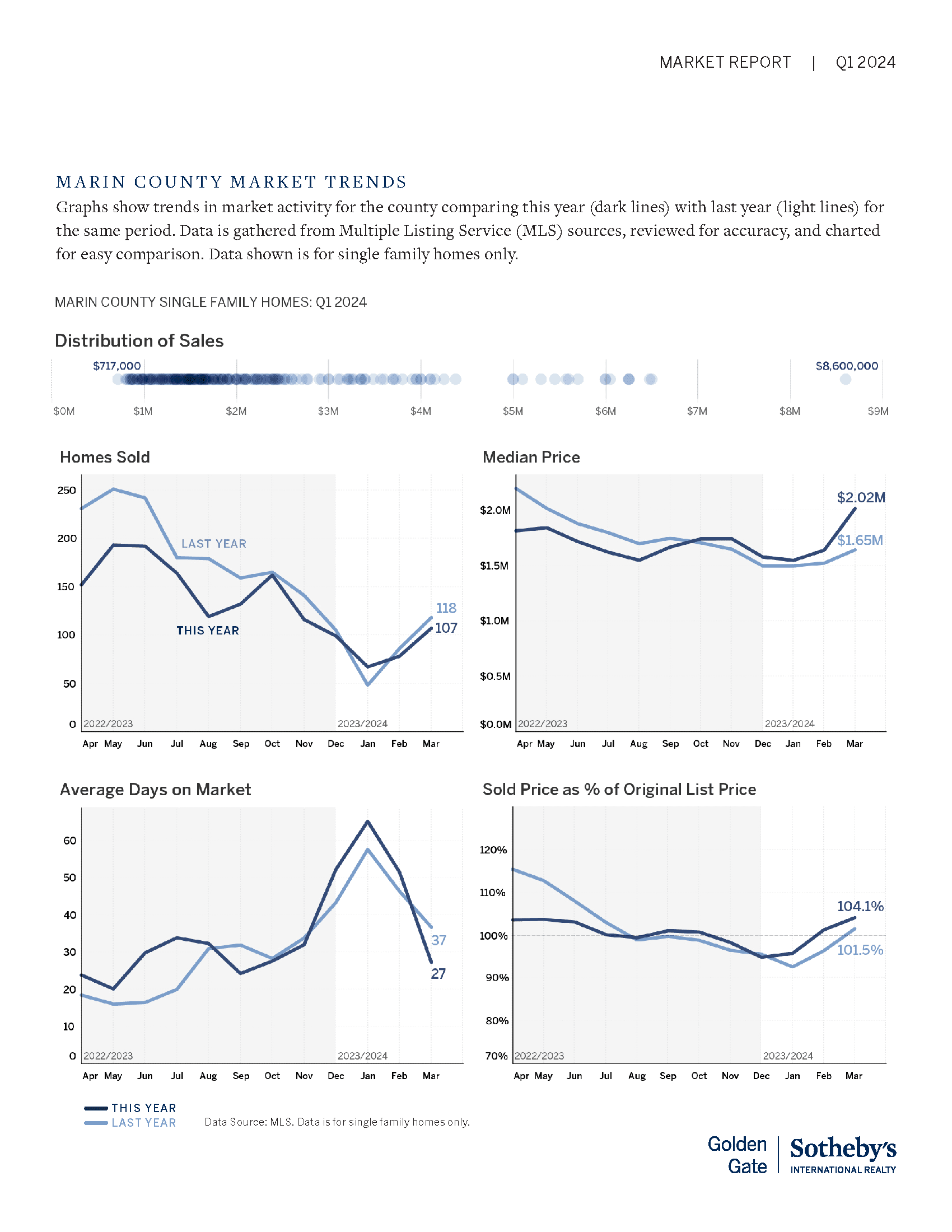

The SF Bay Area housing market gained additional momentum heading into the spring buying season. More homes came onto the market, giving potential buyers additional options in prime neighborhoods. With mortgage rates coming down from the late 2023 high point, buyer activity started to accelerate. Home prices also increased during the first quarter in most areas.

In addition to the strengthening housing market, the economy made moderate gains. Job growth was strongest in the educational and health services sector, which offset some losses in the technology industry. Though the overall tech sector is not generating as many new jobs as in recent years, the scale and number of layoffs in the SF Bay Area continued to slow. The unemployment rate increased slightly to 4.3%, though a figure less than 5% indicates a tight labor market. Fewer tech layoffs and continued record-setting performance of stocks should bolster the housing market into the remainder of the spring and summer buying season.

FOR-SALE INVENTORY EXPANDS

Pricing trends as well as moderating mortgage rates helped convince a growing number of homeowners to list properties for sale. In the first quarter, the number of active listings increased by 15%. This was the largest number of homes for sale in a first quarter since 2019 and inventory increased across all SF Bay Area counties. The most rapid increase compared with one year ago was in the inner SF Bay Area, led by Marin and San Francisco counties.

SALES RISE YEAR-OVER-YEAR

Sales activity was up modestly from the previous year to roughly 7,000 homes sold across the SF Bay Area. Growth in the number of sales was especially strong in San Francisco and Santa Clara counties, where sales increased by more than 10%. Within the first quarter, sales in March outpaced the first two months.

However, compared with one quarter ago the number of closed sales declined by 17%, in part due to the slower January and February activity. From the prior quarter, sales activity held up better in Contra Costa, Santa Clara and Solano counties, while sales declined most rapidly in counties on the west side of the bay.

UPPER PRICE TIERS LEAD THE WAY

Sales activity was mixed across price tiers during the first quarter of 2024, with the upper pricing ranges generally outpacing the most affordable segments. The number of homes sold for more than $3.5 million increased by more than 40% compared with the first quarter of 2023. Additionally, the number of homes sold for $1.25 million to $3.5 million increased by nearly 20% year-over-year. Strong sales activity in the inner SF Bay Area markets was the primary driver of growth in these upper price tiers, most notably Santa Clara County.

Once again highlighting that market conditions improved within the first quarter, sales in the $3.5 million to $5.0 million price range increased by 13.3% from the fourth quarter. The number of sales in this tier doubled from February to March, reaching the highest monthly level since mid-2022.

LOOKING AHEAD

Pent-up demand for housing and an increasing supply of homes for sale should continue to bolster SF Bay Area home sales. The relatively strong economy combined with a modest increase in households moving into the SF Bay Area will support the potential for a greater number of sales. Should mortgage rates decrease further, more buyers will come off of the sidelines. The accelerating pace of sales should continue to drive pricing higher in many neighborhoods. In particular, neighborhoods with a combination of good schools and shorter commutes or access to transit will continue to outpace the broader market. The positive momentum generated during the first quarter, particularly when compared to other regions across the country where prices declined, bodes well for a stronger remainder of 2024.